27 April 2026 Written by Lawrence Liang

Buying Your First Home: Private Sale vs Auction - How Are They Different?

Searching for your first home in Victoria is exciting — but the moment you find a property you love, a very practical question hits you: "Is this going to auction, or is it a private sale — and what does that actually mean for me?"

The answer to that question changes everything: how you prepare your finances, when you need the Section 32 review done, what conditions you can include, and what right you have/do not have.

This guide cuts through the confusion and explains both methods in plain language, so you can approach your property purchase with clarity and confidence:

How Private Sales Work in Victoria

A private sale (also called a private treaty sale) is where a property is listed at an asking price and you make an offer to the vendor through the selling agent. Mostly for high rise apartments in Melbourne or metropolitan areas (Southbank, Box Hill etc) or houses in regional areas such as Ballarat or Bendigo. Negotiations happen behind the scenes, typically through the agent, until both parties agree on a price and terms.

Here's what you need to know.

Understanding The Cooling-Off Period — Your Safety Net

One of the biggest advantages of buying via private sale in Victoria is the cooling-off period. Once you sign the Contract of Sale, you have three business days to change your mind and withdraw from the purchase.

According to Section 31 of SALE OF LAND ACT 1962 (Vic), a purchaser under a contract for the sale of land signs that contract he/she may at any time before the expiration of three clear business days after he/she has signed the contract give written notice to the vendor that he/she wishes to terminate the contract.

However, the cooling-off period does not apply to property that:

is used primarily for industrial or commercial purposes; or

is more than 20 hectares in size and is used primarily for farming;

The cooling-off period also does not apply to below circumstances:

the purchaser bought the property at a publicly advertised auction or on the day on which the auction was held; or

within 3 clear business days before a publicly advertised auction was to be held; or

within 3 clear business days after a publicly advertised auction was held; or

the purchaser and the vendor previously signed a contract for the sale of the same land in substantially the same terms; or

the purchaser is an real estate agent within the meaning of the Estate Agents Act 1980 or a corporate body;

There are a few important catches, however:

If you exercise your right to cool off, the vendor is entitled to forfeit $100 or 0.2% of the purchase price (whichever is more) from your deposit. On a $650,000 property, that's $1,300 — not nothing, but far less painful than being locked into a purchase you do not like.

Pro Tip: The cooling-off period is a safety net, not a strategy. First home buyers often think they can sign the contract first and "cool off later if needed." Don't do this. Always have the Section 32 and Contract of Sale reviewed by your conveyancer before you sign.

Protective Conditions

Unlike auctions, private sales allow you to include conditions in the Contract of Sale subject to vendor’s approval. These conditions are some common ones:

Subject to Finance: Allows you to exit the contract if your home loan is not formally approved by your lender within a set timeframe. This is particularly important if you are using the Australian Government's 5% Deposit Scheme or requiring high Loan-to-value ratio loan (>80%), where lender approval processes can take longer and need a few more boxes to be ticked off.

Subject to Building and Pest Inspection: Gives you the right to withdraw (or renegotiate) if a qualified building inspector identifies major structural defects or pest issues. Given that properties across Melbourne's established suburbs — from Footscray to Frankston, Northcote to Noble Park — can carry decades of hidden maintenance issues, this condition can give you extra peace of mind.

Other terms and conditions: you may negotiate to have a settlement term fits your current lease expiry term. You may also negotiate a lower deposit if some of your savings are tied up in a term deposit high interest earing account. You may also delete additional special conditions added by the vendor.

Pro Tip: For the vendor, an unconditional offer is often more favourable. It can be a good negotiating tactic for a first home buyer to submit an offer with no additional condition. You will have a better chance to negotiate lower price. But remember only go unconditional if your mortgage pre-approval is fully assessed (not just pre-qualified), your building and pest inspection is complete beforehand, and your conveyancer has reviewed the Section 32 and Contract in full. Going unconditional without those safeguards is a costly mistake to make.

How Auctions Work in Victoria

Auctions are a dominant feature of the Victorian property market — particularly in metropolitan Melbourne, where weekend auction clearance rates are closely watched by buyers, sellers, and media alike. Understanding how auctions work before you find yourself standing on a footpath with a bidding paddle in hand is absolutely essential.

Auctions Are Unconditional

This is the single most important thing every first home buyer in Victoria must understand about auctions: if you are the successful bidder, you are unconditionally committed to the purchase on the spot.

There is:

No cooling-off period

No finance condition — if your bank doesn't come through, you are still legally bound

No building inspection condition — whatever defects exist, they are now your problem

No opportunity to renegotiate after the hammer falls

You sign the Contract of Sale immediately, and you pay the deposit — typically 10% of the purchase price — on the day.

What You Must Do Before Auction Day

Because the auction purchase is unconditional, all of your due diligence must be completed before the auction begins. This means:

Have the Section 32 and Contract reviewed by your conveyancer

The selling agent will make the Section 32 and Contract of Sale available to interested buyers during the campaign — often weeks before auction day. Send these to your conveyancer as soon as you receive them. Unlike a private sale, you cannot negotiate contract terms after the auction, so any concerns must be flagged and ideally resolved beforehand.

Complete your building and pest inspection before auction day

In Victoria, building inspections for auction properties must be arranged by the buyer independently and completed before auction day. Don't assume that because a property looks well-maintained at an open for inspection, it is structurally sound. Hidden defects in plumbing, roofing, foundations, or electrical systems are common — particularly in Melbourne's established suburbs where older housing stock is prevalent.

Know your number (maximum bid) — and stick to it

Arrange pre-approval before so you have the confidence to bid and know the range you can bid up to. It is also worth to find out from your mortgage broker if your pre-approval is fully assessed or system approval. The competitive, public nature of auctions creates a psychological pressure that is very real. Bidding wars in sought-after suburbs like Glen Waverley, Kew, and Toorak can push prices well beyond initial estimates in a matter of minutes. Knowing — and holding — your limit before auction is critical.

What if a property pass in at auction?

If the property passes in — meaning bidding does not reach the vendor's reserve — the highest bidder generally has the first right to negotiate privately with the vendor. This is an important opportunity, but bear in mind that if you signed the contract on auction day, there is no cooling-off period.

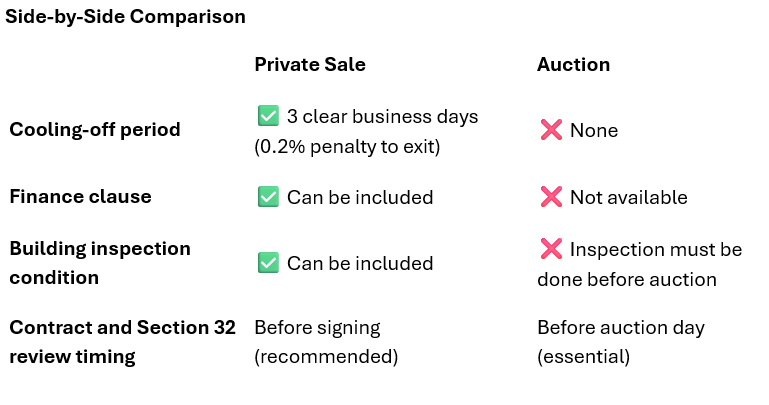

The selling method is set by the vendor. What you can control is how prepared you are for each scenario. Here are some key differences:

Related articles

The information contained in this article is provided for general informational and educational purposes only. It does not constitute legal, financial, or professional advice and must not be relied upon as such.

This information has been prepared without taking into account your individual objectives, financial situation, or needs. You should consider whether the information is appropriate to your personal circumstances and seek independent professional advice before taking any action based on this content. While every effort has been made to ensure the accuracy of the information, no responsibility is accepted for any errors, omissions, or reliance placed on this material.